Help us direct you to the right place to sign up

As we move into the new year, it is time to take a look at the CRE market after another year of change. 2022 brought about the end of COVID-19 as a practical consideration, but also yielded a slowdown in CRE investment amid rising interest rates in response to the highest inflation rates since the 1970s. Last month, we hosted a webinar where our Co-founder and CEO, Michael Mandel, sat down with KC Conway, the founder and CEO of Red Shoe Economics, to discuss the trends that shaped commercial real estate in 2022 and how we can expect CRE markets to evolve in the coming year.

The defining economic trends of 2022 were inflation and the Federal Reserve’s reaction to it. Think back a year ago to December 2021. The stock market had just reached a record high the prior month, and despite an end-of-year pullback, was set for a robust year-on-year gain. The rapid spread of the new omicron variant dashed hope for an end to COVID-19. People were beginning to take note of rapid price rises although major consternation about inflation was mellow.

Take a look at how much can change in a year. Many economists have expressed that there is a high risk of a recession in the near future. Stocks are down year over year. Interest rates skyrocketed and increased seven times throughout 2022. The most recent inflation data covering December 2022 released last week revealed that inflation is decelerating but remains well above the target rate of around 2% annually. Based on the current inflation figures and a stronger than expected pace of hiring in the job market, the Federal Reserve is expected to raise rates again at the next FOMC meeting in late January, though they have signaled they may slow the pace.Although COVID-19 is still around, the related socio-economic phenomena has disappeared from the United States as society has moved on. These vast changes have impacted the commercial real estate market as well.

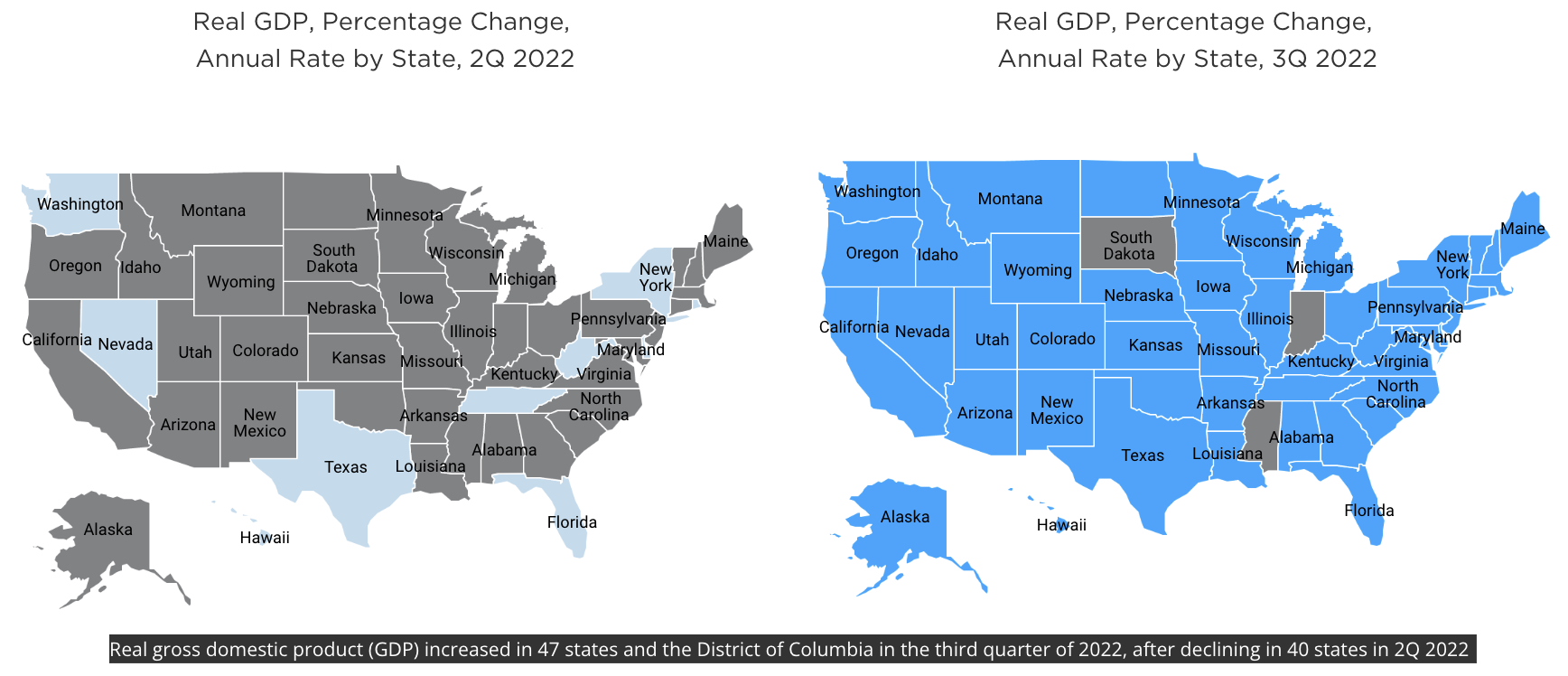

State by state breakdown of GDP growth or decline in Q2 and Q3 2022

Changes in Capital Allocation

Rising interest rates are a blunt tool to reorient the risk-reward calculus across the economy. Commercial real estate is no exception. Rises in interest rates mean that investors can get a decent return with “risk-free” assets like treasuries. As such, they demand higher rates of return from riskier assets. In CRE terms, this means investors are now demanding higher cap rates as the risk inherent in real estate investment is also higher. In tandem, financing terms for CRE deals are getting more stringent as banks are charging higher interest rates and adjusting the debt to value rates for their deals. In other words, the cost of capital has gotten higher.

Funds want less office space and expect office space value decline

A Slow, Soft Market

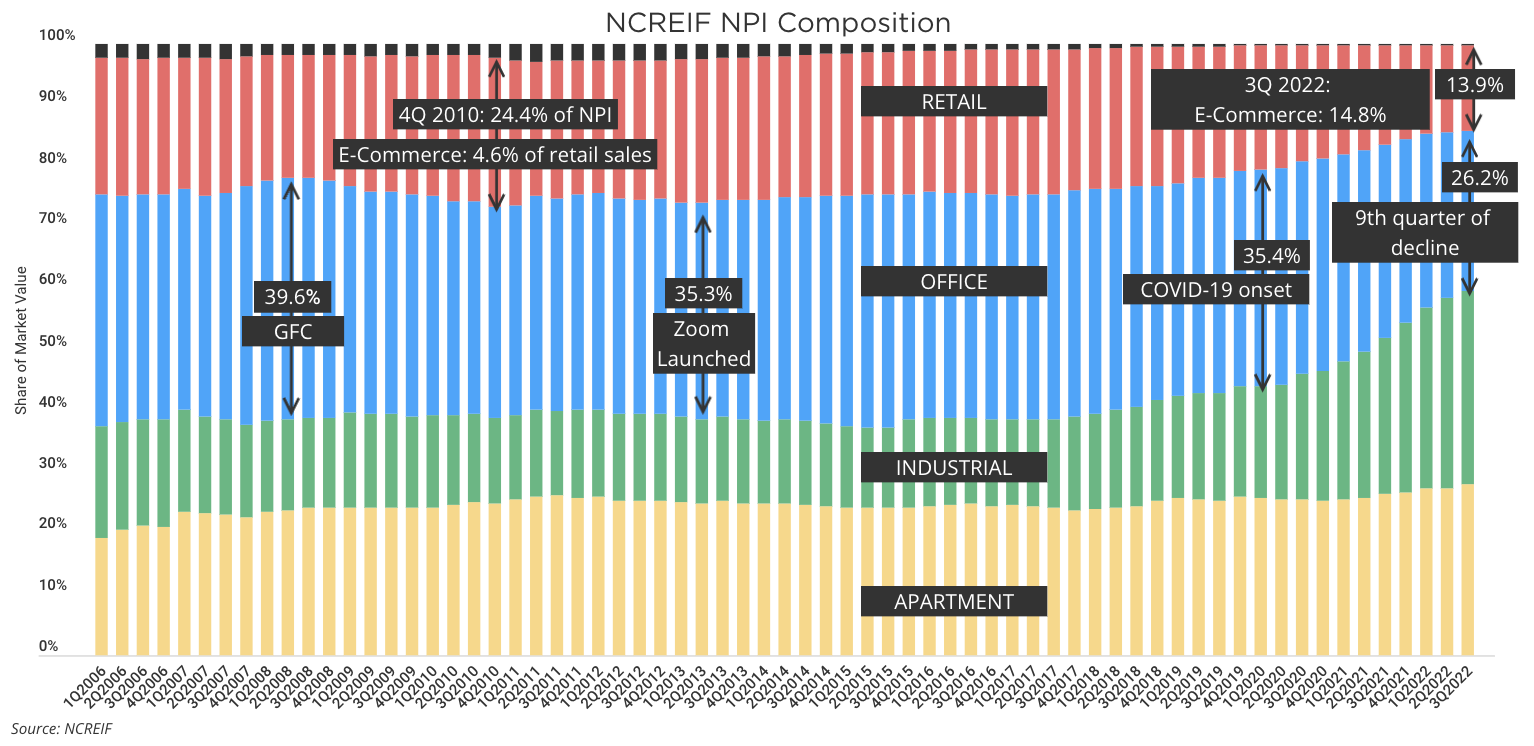

Changes in cap rates mean a fundamental repricing of the real estate sector. Yet few owners want to sell at a significant discount to what they could’ve gotten last year, and there are few buyers eager enough to buy something at full price. Thus, deal velocity has plummeted and the only deals happening are those that absolutely have to happen due to buyer or seller needs. One category of deals that have to happen is large players exiting the office space market entirely. Investors such as pension funds and some private equity investors have decided that the storm clouds on the future of office space look too unpredictable and that it is time for them to get out. The office sector comprised 26.2% of the NCREIF Property Index (NPI) as of the third quarter 2022 and its share has been falling for nine consecutive quarters. Pre-pandemic, office’s share averaged 35.0% during 2019, according to NCREIF and the NPI.

Return to Office No More: The Post COVID-19 New Normal

Throughout the COVID-19 pandemic, return to office has been a distant hope that would bring the office space market back into equilibrium. Industry players hoped that offices would fill back up once everyone was vaccinated and COVID-19 was “vanquished”. The most vocal supporters of “return to office” explained that Industries and companies could not function without the collaborative and social benefits of in-person work. However, most now concede that a full scale return to pre-pandemic office culture and office space demand is off the table. American society has collectively said COVID-19 is over, at this stage worker concern about spread is no longer an excuse for why offices remain vacant. COVID-19 has brought up something unexpected in the American work culture — a meaningful chunk of employees and employers that have decided they need less office space or no office space at all.

Beneath the surface, things may be worse than they seem for commercial office space markets. Most leases have yet to come up for renewal since COVID-19 hit. As each year passes, a meaningful number of leases may be dropped or downsized at renewal time. We can see evidence of this in so-called “shadow space” – office space that is leased and paid for, but that tenants do not need or fully utilize. Shadow space tenants would gladly sublease their office space or would leave if the landlord let them. With a short remaining lease term, it is often not worth the effort for these tenants to find a sublessee. These tenants represent a latent unrealized excess capacity in the office space market that could further depress the market once these leases roll over.

Comparing SF and NYC Office Markets

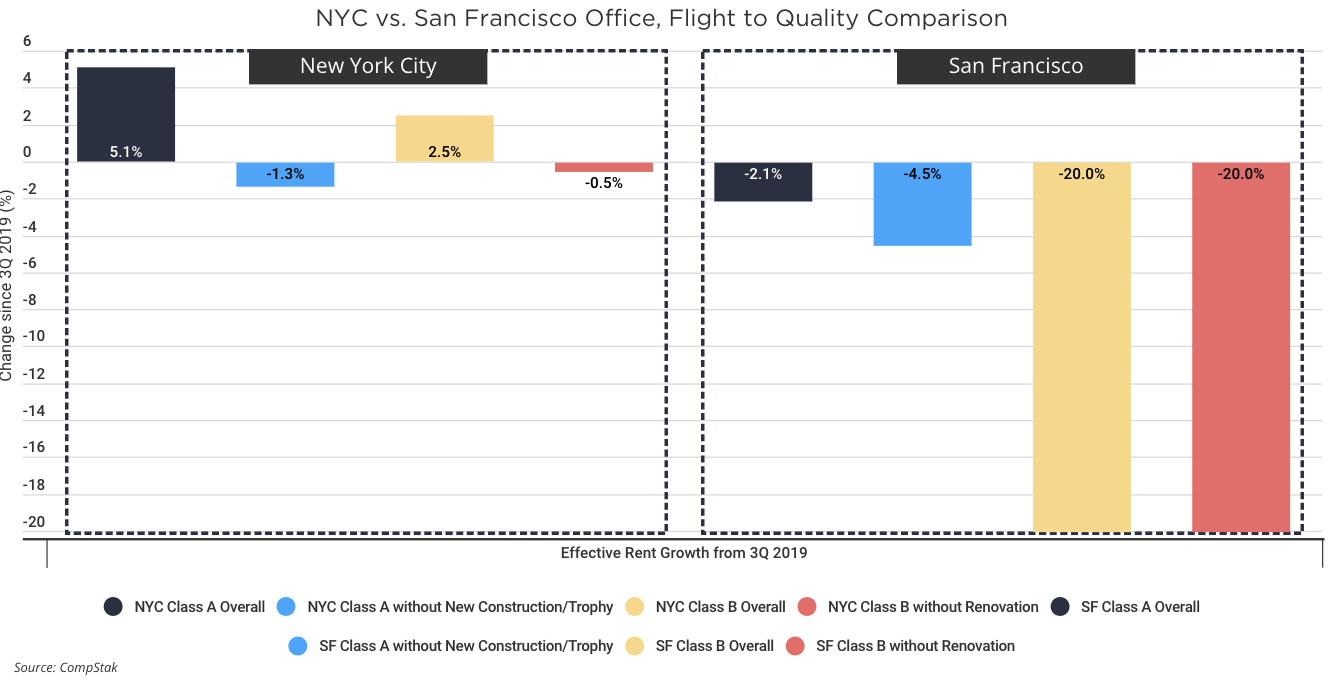

The impact of lease rollover can be seen in individual market dynamics. Office space rents are down substantially more in San Francisco than in New York City. One could ascribe this to the different work cultures of the cities or a different composition of industries leasing office space. But the answer is simple: San Francisco leases are traditionally much shorter than New York leases, so a larger share of San Francisco office space leases have rolled over since COVID-19 whereas only a smaller proportion of New York leases have done so to date. For example, in 2019, New York City’s lease term averaged 82.0 months as compared to San Francisco’s 57.6 months, based on CompStak data. The same dynamic is apparent if you divide leases by office space class—Class A transactions were on average 13.6 and 18.9 months longer than Class B deals in San Francisco and New York City, respectively in 2019. Effective rents for Class B leases have dropped much more steeply than Class A leases in San Francisco, in particular. Again, the answer may lie in the lease term — Class A leases are traditionally long leases inked by blue chip firms, whereas Class B leases are shorter on average and dominated by smaller firms. Far more class B leases have rolled over; hence the steeper drop in price. However, in San Francisco, Class A effective rents are still down from pre-pandemic levels while New York City has experienced an increase almost entirely due to leasing in new construction. In San Francisco, Class A leases may have further fallen as many of the tech firms that drove the growth in the office market over the past decade have recently suffered major drops in the stock market and announced hiring freezes or downsizing. Even though firms like Amazon and Google knew that remote work would dampen the need for office space, they planned to expand so rapidly that even with a smaller portion of their workers choosing to work in the office they needed more desks. This is no longer the case. Stay tuned – we’ll more be diving deeper into NYC and San Francisco office markets in our upcoming research report with our partner, Trepp.

Although we are yet to fully understand long-term impacts of COVID-19, raising interest rates, supply chain issues, remote work, and other factors, we can rely on high-quality, relevant data to keep up with the market dynamics. Many of us didn’t expect how the past few years are going to change the way we work, travel, and do business. Stay with CompStak to keep a pulse of the market and make sure you never miss new CRE trends!

Want to watch the webinar replay? Check it out below and subscribe to our YouTube channel!

View the webinar slideshow below and click to download your copy

QA with Michael Mandel, CEO and Co-Founder of CompStak, and KC Conway, Principal and Co-Founder of Red Shoe Economics

Q: What does an increase in rents in renovated Class B buildings in NY mean for CRE versus a 20% drop in rents for Class B Space in San Francisco?

A: (Michael Mandel) I would speculate that you will see a difference in San Francisco where you’re going to see a worse impact to the Class B buildings that haven’t been renovated versus those that have. And generally that’s going to be the major indicator as to where the hurt and the pain is felt. I think that you’re going to see more pain in the buildings that haven’t been renovated. It’s important to note that flight to quality is not just moving from one building class to another. Flight to quality also means moving from quality space within a building class.

Q: What can we take away from how we performed on Black Friday and over the past few months?

A: (KC Conway) The headlines were that retail traffic was up, like 7%, but the retail traffic to conversion of sales was actually down 7%. CoreSite has a new metric that they’ve been following which is the cancellation rate in ecommerce carts. And so you go back six months to a year ago and the typical cancellation rate was about 10%. What they found recently is the cancellation rate has gone to 75%. That tells you how concerned we should be on the ecommerce side of what’s happening with retail sales.

Source: Coresight.com. Coresight Research shows that the average 12-month online cart abandonment rate on retailer’s websites is 75.7%.

Q: We talk a lot about Class A vs Class B office space. How is that defined exactly?

A: (Michael Mandel) That’s a really interesting question because there is no official definition for Class A, B and C. It’s not like you can look this up from any source and say, this is what makes it so. In our case we’ve crowdsourced the classes of properties, and so we get that from our members, and of course, if a building gets renovated and upgraded, and maybe would be considered to be in a new class, we’ll start hearing that from our members through crowdsourcing. But what we found obviously is that there are very strong trends in the data underlying those building classes. So9 we can use those to extrapolate what a class should be based off of the underlying rents and building quality. In the cases where we don’t have a crowdsourced building class, we actually arrive at a building score which we then translate to class. And what impacts that comes from the market rent in the property, the number of leases in the proximity, the property size, the year the building was built, the number of floors when the building was renovated.

Q: What does the medical office look like in this economy?

A: (KC Conway) There’s a lot of good fundamentals in things like medical office, industrial, suburban, retail, even multifamily, but where’s the capital going to come from? So I think that’s the biggest challenge, not the fundamentals, particularly in medical office, but really where’s the capital going to come from? And what that means is that more expensive capital means debt is higher and equity is higher. You put those together, you get a higher cap rate. It’ll be worse on some property types, I think particularly office, but it’ll be less severe in industrial or medical office because you can probably grow into an aggressive cap rate with the rents going up.

Q: Do you see a potential impact to New York City revenues if assess values keep going down in commercial space?

A: (Michael Mandel) We absolutely would expect an impact to New York City revenues, and not only would we expect it, but the city of New York recently came out with a report from the Independent Budget Office, saying exactly that. So they are concerned about New York City revenues from commercial real estate. They expect commercial and residential sales to rise by the 2025 fiscal year. They are expecting that in the near term the cooling real estate markets are going to impact tax revenues for fiscal year 2023, and they’re concerned about no growth or negative growth in the near future. They do forecast that rents will ultimately increase going into 2,026 but high availability in the near term will keep rents lower.

Q: Everyone is talking about possible economic gloom and doom. For the realtor folks, how do you sustain a healthy business during this stage? Where is the opportunity?

A: (KC Conway) I think the first thing has to be that there is gotta be a recognition that there’s going to be fewer transactions. So the federal reserve just raised another 50 basis points. That means the debt costs are going to be higher and transaction costs are going to be harder to make work with the debt service. Fewer transactions means you have to do a better job of screening what you work on.

It also means that there’s a bigger disconnect between buyers and sellers. Right now, sellers are still holding on to their properties that are worth what they were a year ago at 4 and 5 cap rates and haven’t come to recognize what buyers are recognizing – which is, we’re going to apply a 6, 7, or 8 cap rate, and that means 20-30%.

And then look at your business. If you’re doing a lot of office leasing in downtown markets, I think that office faces more headwinds than say other property types like an industrial and multifamily. So you may have to pivot there and you may have to expand your geography.

Related Posts

Midtown Finance and Legal Tenants Reigned Supreme in Top Ten Manhattan Office Leases by Value in 2024

Midtown Finance and Legal Tenants Reigned Supreme in Top Ten Manhattan Office Leases by Value in 2024

CompStak Portfolio Series: BXP, Inc. vs. Perform Properties