Help us direct you to the right place to sign up

SKIP AHEAD TO

The last few months have seen major shifts in macroeconomic conditions. Inflation has hit a level not seen since the 70s, and the Fed has belatedly sprung into action with a series of interest rate increases. These changes have ricocheted throughout the economy and commercial real estate is no exception. How is the CRE market adapting to this new reality?

CRE Landscape

Let’s first set the scene. The last few years have been a wild ride as the COVID-19 pandemic supercharged changes in the way we work, shop, and live. The rise of online shopping and robust consumer demand for durable goods spurred on by economic stimulus and limited recreation dramatically increased demand for industrial real estate. In contrast, the advent of widespread remote work, and its unexpected staying power, softened demand for blue chip office space. The CRE landscape shifted as demand for industrial real estate skyrocketed, and cap rates in the sector plummeted to more closely resemble multifamily real estate, the traditional safest CRE asset class.

Inflation and Rising Interest Rates

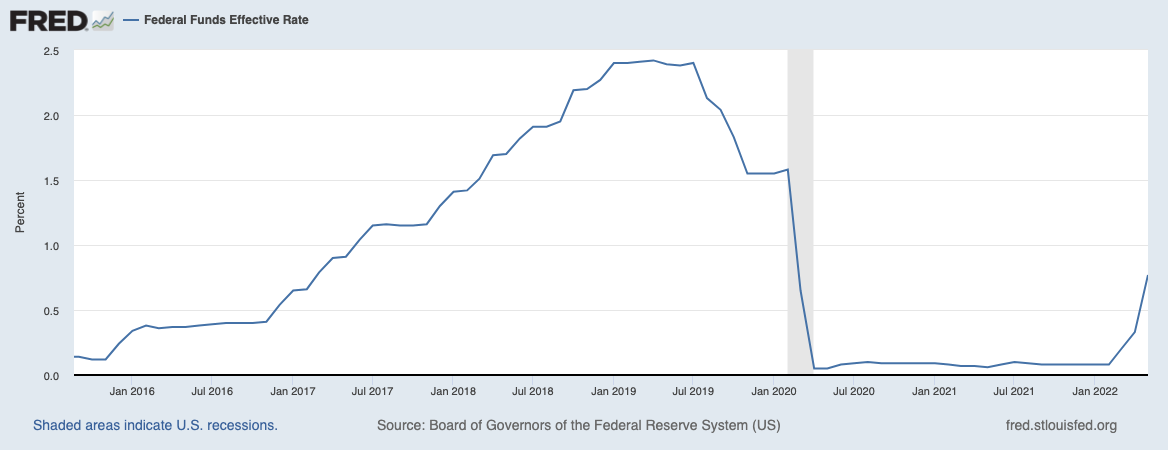

Fast forward to today. The Fed has responded to inflation by trying to cool the economy with rising interest rates. These efforts have already yielded an effect: this April, for the first time in over a year, CRE sales were down on a year over year basis — by 16%. This reversal is quite sudden, paralleling the rough spring capital markets have experienced as just a month before April’s decline, in March, sales were a healthy 57% above normal.

Inflation, consumer prices for the United State Source: https://fred.stlouisfed.org/series/FPCPITOTLZGUSA Inflation, consumer prices for the United State Source: https://fred.stlouisfed.org/series/FPCPITOTLZGUSA |

The causes of this slowdown are twofold. For one, CRE investors have adopted the same pessimistic attitude that the rest of the market has. Rosy outlooks have been replaced by forecasts of recession, reduced demand, and an economic cooldown. The second is more interesting. Interest rates have surged in recent weeks, and investors are now stuck with the unhappy surprise of substantially more expensive loans. Given the central role that debt financing plays in CRE investments, this sudden change has forced a reassessment of what is and isn’t worth it. Events so far have been ominous for the state of the CRE market as a whole. In one particular example, Innovo property group chose to back out of a deal to purchase an office tower at 452 Fifth Avenue in Midtown Manhattan for $855 million rather than go through with a mortgage on substantially less appealing terms.

According to CompStak data, the median industrial starting rent nationally has not yet demonstrated signs of decline or a plateau. In Q1, the median industrial starting rent for transactions above 50,000 square feet nationally was $7.08/SF, up from $6.75/SF at the end of Q4 2021 and up 11.03% year over year. In Q2 to date, the starting rent has continued to climb.

In aggregate, these changes in the CRE market may lead to a transition from a seller’s to a buyer’s market. Deal velocity has slowed and sellers are anxious to get deals done now lest conditions sour further. This may mean a repricing is in order—the unprecedented drop in cap rates in sectors like industrial combined with higher interest rates leaves prospective investors in the sector staring at meager returns. This reduced deal flow may have consequences for rents as well as reduced activity leaves more properties in limbo and constrains the options available to landlords. Where will the market go from here? Get started with CompStak for accurate CRE data and analytic capacities to find out.

Related Posts

Will Rising Interest Rates Freeze The Multifamily Sector?